Testing: The ups and downs of wheel performance when creep-feed grinding - grinding wheels for carbide endmills

Much of the knowledge on how to run PDC bits properly flowed from Shell International Petroleum Co. Ltd.'s research on torque and vibration problems, Amoco's antiwhirl developments, and work by other major oil companies and service companies.

Historically, two factors have been mainly responsible for limiting the operating range and economics of running PDC bits: shortened life because of cutter fracture and slower ROP because of inadequate cutter cleaning.

Another relatively recent advance is the use of polished diamond cutters. The polished PDC surface has a significantly lower coefficient of friction, preventing cuttings from building up on the cutter surface.

As PDC bit design improves, the bits tend to drill longer intervals, and many can be used in several wells. In such cases, footage drilled per bit is more important than the number of bits used.

Improvements in ROP and bit life allow PDC bits to drill harder formations, previously thought drillable only by rock bits or tungsten carbide insert bits.

At about $10,000-150,000 apiece, PDC bits generally cost five to 15 times more than roller cone bits. But a PDC bit run in the proper application can substantially lower total drilling costs despite the higher initial expense.

Designing and building a new bit has become very fast, mainly because of advances in CAD/CAM and engineering practices. PDC bits have become a specialty tool, not a commodity that can be bought in large number in advance of need.

The market for cutting tools is constantly changing, with new business prospects constantly appearing. The increasing need for cutting tools in the medical and dentistry sectors is one of the most recent industry opportunities. The demand for precise equipment that can handle intricate and delicate tasks is growing as technology advances. Orthopedic surgery, neurosurgery, and dental implant placement are procedures that use cutting instruments.

Commercial practical limits for PDC bit sizes have been 31/ 2-in. and 171/ 2-in. diameters. These limits are due mainly to economics, not technology.

PDC bits generally work better in oil based muds than in water based muds. Oil-based muds, however, are not viable options in many areas because of environmental regulations and the high cost of disposal or treatment. As a result, many operators may use water based muds.

PDC bits are most effective in very weak, poorly consolidated, brittle, hydratable sediments -- sands and silts, for example.

Precision cutting tools are in great demand in aircraft, automobile, and medical device manufacture. In addition, advanced materials and technologies like composites and titanium alloys demand precise and efficient cutting tools. Businesses use cutting-edge cutting tools that may relate to robots and other automated systems to optimize output and save costs. Thus, cutting tool technologies like sensors and data analytics allow real-time monitoring and optimization of cutting processes. Sustainability and environmental responsibility also drive demand for energy-efficient and waste-reducing cutting tools. Due to stricter rules and requirements, companies actively seek cutting-edge techniques to reduce their carbon footprint and satisfy ecological objectives.

Key drivers include technological advancements in manufacturing processes, increasing demand from the automotive and aerospace sectors, and the growth of the industrial and construction sectors globally.

BIG KAISER Precision Tooling Inc., Kennametal, Nachi-Fujikoshi Corp., OSG USA, INC., Sandvik AB, Ceratizit S.A., Dewalt, Fraisa SA, Guhring, Inc., Kilowood Cutting Tools, Xiamen Golden Egret Special Alloy Co. Ltd., Zhuzhou Cemented Carbide Cutting Tool Co. Ltd., Tiangong International Co., LIMITED, Ingersoll Cutting Tool Company, Sumitomo Electric Hartmetall GmbH, Kyocera Unimerco, and ISCAR LTD and Others.

The new bit drilled 1,338 ft in 145.8 rotating hr for an average ROP of 9.2 ft/hr. The two bits run in the offset well drilled a total 1,017 ft at an average ROP of 6.3 ft/hr.

Furthermore, the cost of tungsten carbide, used in the stud that holds the diamond, has increased during the past few years.

Several service companies and operators use rock strength analysis computer programs to determine the hardness of formations in a well. These computer models use well log analysis techniques and empirical formulas to determine the confined compressive strength of formations to be drilled.

The biggest change in the PDC bit industry was identification of bit instability, or bit whirl, by Amoco and the subsequent antiwhirl bit designs. Basically, bit whirl is any deviation of bit rotation from the bit's geometric center.

Hughes Christensen has formed many successful alliances with operators. Many of such alliances focus on a technical objective.

Bit performance economics are measured in terms of cost per foot drilled. This involves factors such as bit cost, footage drilled, time spent drilling, trip time, and daily rig costs.

If the price premium for a PDC bit is less than the value of the saved drilling and tripping time, the PDC bit will be the most economic choice.

Many operators still prefer to choose the bit themselves, usually with assistance from the manufacturer. Manufacturers agree that the most prudent method is to choose a bit based on the interval to be drilled, not on purchase agreements or inventory on hand.

The automotive industry significantly influences the market as it requires precise and efficient cutting tools for manufacturing complex components. The push towards electric vehicles (EVs) is also driving demand for specialized cutting tools.

Some of today's PDC bits can drill entire intervals that required two to three PDC bits or five to 10 roller cone bits only a few years ago. The big advantage comes in reducing the number of bit trips and increasing penetration rates, especially for deep wells or those with high rig costs.

Exeter received proprietary rights to the bit, and Hughes Christensen developed a new bit it could manufacture for costs similar to that of old style bits.

Furthermore, operators in the U.S. still drill many shallow wells. So the ability to reduce the number of trips or trip time is not as significant as in deeper wells.

PDC bit design improvements are driven by research, good engineering practices (finite element analysis, accurate analysis of dull bit grading, rock strength analysis, and the like), and fierce competition from other PDC bit manufacturers and the rock bit industry.

Drilling and milling tools often employ high-speed steel (HSS). HSS tools resist high temperatures, making them ideal for stainless steel cutting. Due to their great temperature and wear resistance, ceramics like aluminum oxide and silicon nitride are becoming desirable cutting tools. Turning, milling, and drilling require ceramics. Super abrasives like PCD and CBN are used to process hard and complex materials in cutting tools. Aerospace and automotive production benefits from their wear resistance, thermal stability, and accuracy.

General Electric introduced PDC in 1973. Bits with PDC cutters became commercially available the following year.

Engine, gearbox, and body panel output employ cutting tools. Cutting tools are also significant in aerospace and defense. Machining titanium alloys, nickel alloys, and composites need high-precision cutting tools. Due to the rising demand for aircraft and defense equipment, the aerospace and defense industries will require more cutting tools. Construction uses a lot of cutting equipment, especially drilling, sawing, and grinding. Construction, especially in emerging nations, will likely fuel the demand for cutting tools. Cutting tools also serve the wood sector. Wood uses cutting, shaping, and drilling tools. Furniture and other wood goods will likely fuel demand for cutting equipment in this market. The cutting tools market's application segment shares vary by industry and growth prospects. Due to their strong need for precision machining, the automotive, aerospace, and defense industries will continue to demand cutting tools.

Some operators and manufacturers work together informally, usually to improve bit design by adding specific features to suit a given formation.

Emerging trends include the adoption of advanced coatings to extend tool life, the use of AI and IoT for predictive maintenance and tool management, and a shift towards sustainable and environmentally friendly manufacturing processes.

Larger hole sizes are generally thought uneconomic for PDC bits because large holes are typically shallow and easily drilled by roller cone bits. The high cost to manufacture such large PDC bits usually is not justified. One operator in South America, however, used recently 26-in. PDC bits with success.

The rock strength analysis programs help an operator better determine PDC drillable intervals, make the optimum bit selection, and select appropriate drilling parameters. Such programs have been instrumental in expanding the number of formations drillable by PDC bits.

Cost of the bit may be only about 2-3% of total well cost, yet the bit can affect up to three-fourths of the total cost.

However, the growing prevalence of cutting tools in many industries like automotive, aircraft, and others is leveling up the market shares in North America.

Advances in metallurgy, hy- draulics, and cutter geometry have not cut the cost of the bits. Rather, they have allowed PDC bits to drill longer or more effectively in a greater number of formations. Another key advantage of these design improvements is the ability of PDC bits to withstand hard formation stringers.

Cutting tools shape metal, wood, plastic, and other materials. These hand-held or piston-powered instruments serve a purpose in many sectors. Saws, drills, reamers, taps, end mills, lathe tools, milling cutters, and grinding wheels are cutting tools. Material, finish, and precision determine the cutting tool. Due to a growing demand for high-quality, precise instruments that could boost productivity and efficiency, the cutting tools market is a sector of the economy expanding quickly. In addition, cutting tools have improved in sophistication, tensile strength, and efficiency with the introduction of new technologies and materials.

Metalworking processes frequently employ indexable inserts, including turning, milling, and drilling. They are composed of a tiny cutting edge attached to a larger substrate made of steel or another material, usually made of another hard substance like ceramic or carbide. With indexable inserts, fewer frequent tool changes are required, and efficiency is increased. The cutting edge may be shifted as it becomes worn or damaged. On the other hand, solid round tools are single piece cutting tools produced from a solid piece of material like high-speed steel or carbide. They are employed in several tasks, including drilling, boring, and reaming. Solid round tools are used in high-volume manufacturing processes because of their dependability and accuracy.

Cutters are no longer limited to a 13-mm round shape. They come in various sizes (8 mm to 19 mm) and shapes. A few companies have had success with dome shaped cutters.

Improvements in computer aided design and computer aided manufacturing (CAD/CAM), along with improvements in dull bit grading, allowed optimization of bit design for specific applications.

In general, positive displacement mud motors last longer during drilling. Therefore, bits have to be robust to keep up.

PDC bits usually have applications when long on-bottom times are important, oil-based muds are used, or water-based muds are used in nonhydrating formations. PDC bits also are advantageous for high rotational speed drilling, such as with a turbine or mud motor, or for drilling deviated hole sections.

To meet market demands for precision and effectiveness, companies must engage extensively in R&D, which may be costly. Cutting tools' competitiveness in the marketplace is another key constraint. E-commerce and globalization have given purchasers a wide selection of suppliers and options, making it harder for manufacturers to differentiate themselves and keep market dominance. Manufacturers must spend money and time on branding, marketing, and customer service to compete. 3D printing and additive manufacturing allow the fabrication of complicated parts and components that were hard to make with traditional cutting tools, impacting the traditional tools for the cutting business. Cutting tool makers must adapt to new technologies and combine their products with 3D printing and additive manufacturing. Finally, the global scarcity of competent labor restrains the cutting tools industry. There are fewer competent employees to operate and maintain modern cutting tools as demand rises. Manufacturers must train and retain skilled people, which is tough and expensive.

These bits, most of which use PDC cutters, generally drill the more critical, expensive wells around the world. Diamond bits account for almost one third of the world bit market, and sales exceed $200 million/year, the U.S. Department of Energy reports.

Although most PDC still comes from General Electric and De Beers, several smaller companies have begun making high quality diamond wafers. This increased competition has not reduced cutter cost, mainly because PDC manufacturing is an expensive, capital intensive process.

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

The technology to minimize downhole vibrations has yielded longer bit life, faster penetration rates, and reduced drilling costs.

Operators and bit manufacturers have developed many ways to prevent bit whirl and overcome or minimize it when it shows up.

This diamond/tungsten carbide interface can be made successfully with various geometrical shapes, instead of conventional flat surfaces, to reduce stress on the diamond face during drilling. As these premium cutters wear, there is more diamond remaining on the stud to continue cutting. This nonplanar geometry has significantly lengthened cutter life downhole.

The typical product life is about 2 years, and the number of variants of a particular design are increasing rapidly.

Hughes Christensen(27064 bytes) predicts diamond bits will account for almost 25% of world footage drilled by 1997. About 10 years ago, PDC bits had only 10% of the market.

Some of General Electric's original PDC patents expired during the past few years, opening the market to many small PDC manufacturers.

Cemented carbide is a popular cutting tool material due to its longevity, hardness, and strength. Turning, milling, drilling, and threading employ it. Hence, the cemented carbide segment prevails in the cutting tools market.

The expanding need for cutting tools in the aerospace sector represents another market potential. Tools that can work with unusual materials, such as titanium, aluminum, and composite materials, are needed in the aerospace sector. The move toward lightweight materials also drives the desire for cutting tools that can make accurate and clean cuts. In addition, cutting tool manufacturers now have new business potential in the renewable energy industry. Tools that can handle the materials used in these applications are becoming increasingly vital as the demand for wind turbines, solar panels, and other renewable energy technologies rises. The parts of these technologies, such as the blades for wind turbines, are produced using cutting tools. Finally, the demand for cutting tools that can be used with cutting-edge manufacturing technologies like CNC machines and robots is being driven by the rising trend towards Industry 4.0 and automation. Cutting tools with improved geometries or specialized coatings optimized for these technologies are in great demand.

Round cutters with a buttress or beveled edge have significantly improved PDC bit performance in several areas. These cutters have worked well in applications in which cutting elements are subjected to high impact loads, such as in hard formations, dynamically unstable drilling, or highly interbedded formations.

Bit whirl patterns can cause the PDC cutters diamond table to chip or spall, accelerating wear and decreasing bit life.

PDC bits historically have found applications in relatively deep or expensive wells and in soft to medium hard formations. In these wells, the longer bit life, compared with roller cone bits, usually offsets the greater bit cost. ROP ultimately determines the economics of the bit run.

Even though PDC bits may be considered a specialty tool, their use is still governed in most instances by economics. The decision to run a PDC bit often focuses on cost per foot or total well cost.

There is no single solution to hydraulics problems at the bit. Each company has a slightly different technical perspective. The goal is to clean the bit effectively but not to erode it with mud flow through nozzles.

We value your investment and offer free customization with every report to fulfil your exact research needs.

Sources such as service companies, operators, vendors, and investment bankers use various methods to gauge the success and growth of PDC bits in the drilling industry. Some market analyses include the number of bits sold or purchased, footage drilled per bit, or bit revenue.

Today's PDC bits drill about 1 1/ 2 times faster than comparable PDC bits in use only 2 years ago. The polycrystalline diamond now used is about twice as abrasion resistant as the diamond used 2 years ago. Many of these types of improvements are considered fine tuning or evolutionary changes in design.

The last true revolutionary change in PDC bits occurred in the late 1980s after Amoco Production Co. identified bit whirl, an inefficient mode of drilling. New bit designs and changes in drilling parameters to combat bit whirl have drastically improved bit life and rate of penetration (ROP).

In one case, Exeter Drilling Corp. and Hughes Christensen formed an alliance to design a PDC bit that would drill wells in the Denver-Julesberg basin of the Rocky Mountain region fast but with reduced pump pressure. They codeveloped a 77/ 8-in. multiport PDC bit that drilled more than 75,000 ft without repair, averaging 103.2 ft/hr.

Each manufacturer has a slightly different design concept, and no one design seems to stop or prevent whirl in all situations.

One of the biggest limitations on high penetration rates is the need to avoid overheating the PDC. The PDC wafer and tungsten carbide base have different coefficients of thermal expansion, which can lead to cracking at high temperatures.

Sandvik AB, Kennametal Inc., Robert Bosch GmbH, Stanley Black & Decker Inc., Mitsubishi Materials Corporation, OSG Corporation, Kyocera Corporation, Guhring KG, ISCAR LTD and Seco Tools AB are some of the major companies in the global cutting tools market.

For example, Enron Oil & Gas Co. and Diamond Products International have such an agreement in which Enron helped design a new PDC bit for an area in the Gulf of Mexico where PDC bits have been used successfully for years. Although previous PDC bits worked well in the area, changes in hydraulics design, cutter layout, and blade spiraling increased penetration rates 20-30%.

What's more, design improvements have allowed PDC bits to drill harder formations and soft formations with hard stringers, previously thought to be drillable only by roller cone bits.

The bottom hole pattern (left) of a whirling PDC bit has an irregular pattern, whereas the bottom hole pattern (right) of an antiwhirl PDC bit shows smooth drilling.

About 75% of the PDC bit market lies outside the U.S., say Diamond Products International Inc. and Security DBS. Many non-U.S. areas have relatively soft formations or are expensive to drill because of high rig day rates, remote or offshore locations, or deep wells. Those factors present favorable economics for PDC bit use.

Much of this focus has been on making the diamond layer more abrasion resistant and reducing the stress behind the diamond layer. The bond between diamond layer and tungsten carbide stud is critical for a PDC bit.

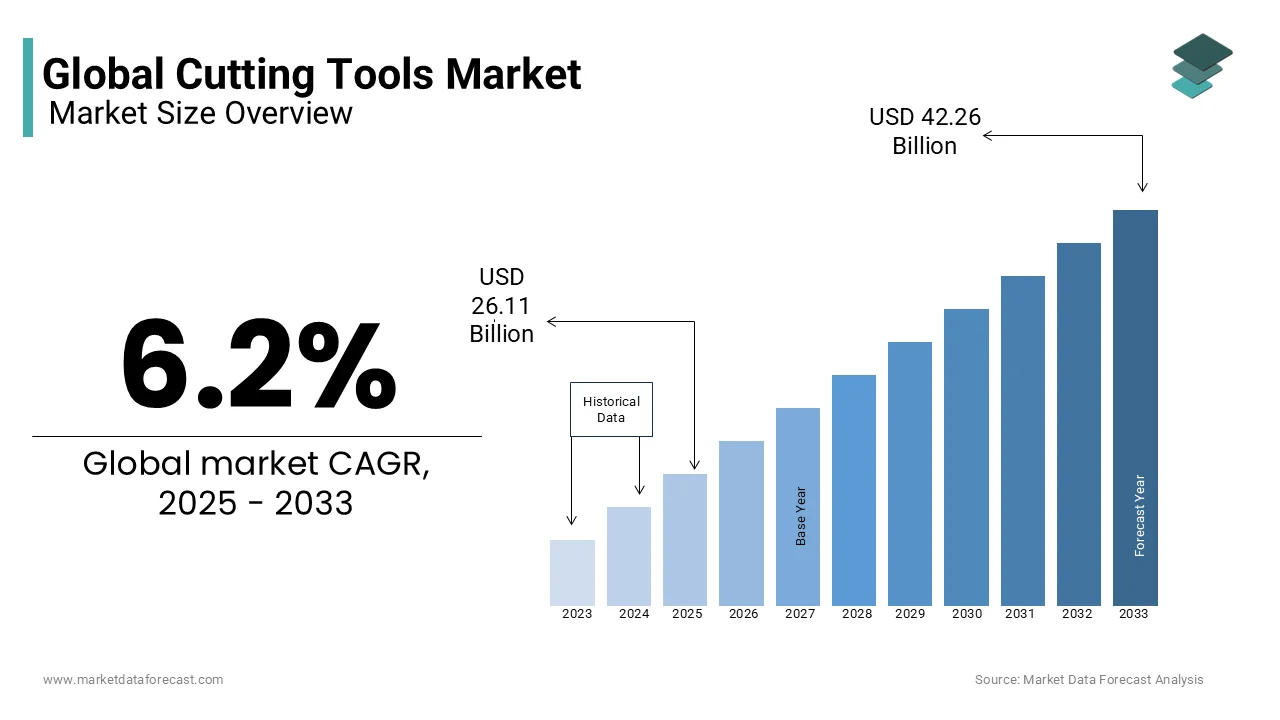

The global cutting tools market is expected to grow at 6.2% from 2024 to 2029 and the global market size is predicted to be valued at USD 24.59 billion in 2024 and increase to USD 33.21 billion by 2029.

BP ran a 171/ 2-in. Hycalog PDC bit on the BA-X14 well in Colombia's Cusiana field, where offset well BA-X11 on the same drilling pad required two PDC bits, one from Hycalog and one from another manufacturer, for the same interval

Some new synthetic muds, based on mineral oils or glycerin, and friction-reducing additives for water base muds have helped improve PDC bit penetration rates compared with that in typical water based muds.

Bit whirl can be caused by cutter/ rock interaction forces and things such as formation characteristics and undesirable bottom hole assembly motions. Conventional PDC bit technology provides little resistance to whirl and may reinforce whirl once it starts.

PDC cutters consist of a layer of bonded diamond particles backed up by a thicker layer of tungsten carbide.

Some operators and manufacturers prefer not to take part in such formal agreements because of the speed with which PDC bits undergo improvements. Bits often are left out of many drilling alliance agreements between operators and service companies.

Recent advances in metallurgy have allowed use of various PDC cutter geometries. These cutters are less susceptible to breakage and can withstand stress better.

Many formations in the U.S. are not well suited to PDC bits. Extremely hard rock and soft formations with hard stringers can often be drilled more economically with roller cone bits than with PDC bits.

As PDC bit use has become more widespread, directional drillers and drilling engineers have become more familiar with the proper operational parameters to run a PDC bit successfully in a given formation. Those parameters include weight on bit, mud pressure, flow rate, and rotational speed.

If peculiar wear is found, that information can be used to alter the design of the next bit. Most manufacturers can then redesign and build the new bit and have it on location almost anywhere in the world within a couple of weeks.

Advances in polycrystalline diamond compact (PDC) bits have sharply increased penetration rates(31588 bytes) in oil and gas wells.

They also can be used in low strength, poorly compacted, nonabrasive, shallow sediments, precipitates, and evaporites -- for example, salts, anhydrites, marls, and chalk -- and in moderately strong, somewhat abrasive and ductile formations such as silty claystone, siliceous shales, porous carbonates, and anhydrites.

For example, BP Exploration Co. (Colombia) Ltd. used only one newly designed PDC bit in place of two other PDC bits to drill an interval in a well in Colombia. It saved $419,000 because of the faster ROP and one less bit trip.

Manufacturing, notably automotive and electronics, has grown in the region, increasing the demand for cutting tools in the market. Major manufacturers in the region are also increasing their market share. Due to manufacturing industry investments, the cutting tools market in Latin America, the Middle East, and Africa is expected to expand. In addition, construction and oil and gas development in these locations will boost cutting tool market size.

Diamond is 10 times harder than steel and twice as hard as tungsten carbide. Diamond also is the most wear resistant material known. It has a wear resistance about 10 times that of tungsten carbide. Diamond, however, is brittle and susceptible to impact damage.

Improvements in PDC bit stability, hydraulics, and cutter design have contributed to increased footage per bit in recent years. Roller cone bits also have shown improvement in performance.

Economic success of the first PDC bits stemmed from high operating costs for the rig and use in very select geological intervals. In the early 1980s, PDC bits underwent true engineering to suit specific field applications.

During whirl, the instantaneous center of rotation of the bit changes, instead of staying in line with the borehole center. Cutters can move laterally and even backwards relative to the local rock surface.

The use of dual powerhead motors, basically two positive displacement mud motors in tandem, has helped stabilize downhole torque. Other improvements in bottom hole assembly components have helped minimize torque and whirl problems.

The market is segmented into milling tools, drilling tools, turning tools, grinding tools, and others. Among these, milling tools hold the largest share due to their extensive use in various applications.

The U.S., by contrast, has many areas in which rig day rates are relatively low, especially onshore. That makes the economics of running PDC bits less favorable.

Some companies use cutter force balancing, bit asymmetry, gauge design, bit profile, cutter configuration, and cutter layout to eliminate whirl. Other manufacturers control whirl through engineered cutter placement designed to create a net imbalance force, pushing against the borehole wall, to create a stable rotating condition.

PDC bits are less effective in hard, cemented abrasive sandstones, hard dolomites, chert, and granites.

18581906093

18581906093